10 Predictions for 2023: No. 7 - More Shareholder Activism & Big Tech Targets

Cheap stocks, overstaffed companies, and a focus on cost-cutting will drive record high investor activism in the tech sector.

(I’m making 10 predictions for 2023. Find the links to my others at the bottom of this post.👇🏿 )

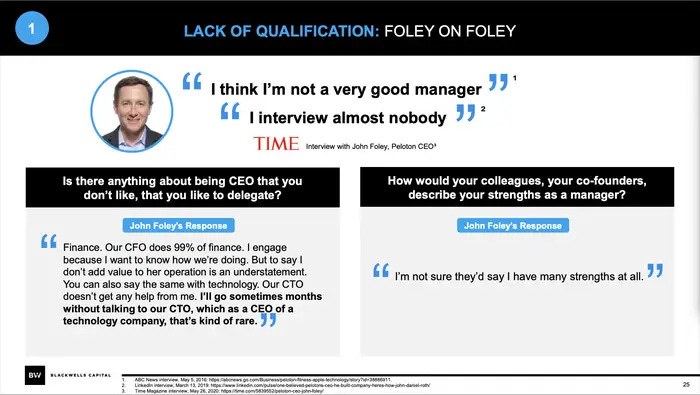

One of my favorite business stories from last year was Peloton and Blackwells Capital.

In February, Blackwells, an activist hedge fund, published a scathing, viral 65-page slide presentation that excoriated the well-known fitness company and its CEO John Foley, all while calling for the company to be sold.

The presentation lambasted the company’s poor stock performance, called Foley unqualified while citing his own words against him, claimed he’d lost credibility, and criticized his personal sales of the company’s stock. At the time, shares of Peloton had fallen more than 80% over the previous year.

The presentation was effective in achieving at least part of its goal. John Foley abruptly resigned as CEO less than two weeks after Blackwells’ presentation was released.

I predict we’ll see more of this in 2023 -- more activist shareholder campaigns with more high-profile technology companies in their crosshairs. Cheap stocks, overstaffed companies, and a focus on cost-cutting will drive record-high investor activism in the tech sector.

As of October, 2022 was on pace to see the highest number of activist campaigns since 2018, according to Lazard.

While 2022’s campaigns largely centered around calls to sell companies or securing representation on their boards of directors, 2023's big tech-focused activism will focus on cost-cutting, overhauling strategy, refocusing on core businesses, and replacing management.

(Boards will continue to be a focus and I’ve also predicted that board governance will be a priority in 2023.)

A few key factors will drive this:

1) Tech companies remain overstaffed, even after layoffs

A meaningful number of knowledge-work jobs, especially at the end of a decade-plus-long economic recovery, are bullshit jobs created primarily to alleviate the self-perceived busyness of managers at overcapitalized companies.

This is no more apparent than in big tech, where Apple, Microsoft, Alphabet, and Amazon, the four largest tech companies by market cap, employ more than 800,000 people in corporate jobs. Of that group, Amazon is the only company to recently announce mass layoffs, but their 18,000 announced job cuts represent a mere 1% of the company’s overall headcount and roughly 5% of its corporate workforce.

As of October of last year, Microsoft, Meta, and Alphabet had all seen their headcounts increase upwards of 20% over the previous year.

As layoffs have surged, the extent of pandemic-fueled overhiring has become more clear:

The chorus of conceding by tech executives that they hired too many people is ricocheting across Silicon Valley as the industry rushes to make cuts, blaming a worsening economy.

But at least part of the surge in layoffs was self-inflicted. When the companies enjoyed soaring profits and a belief that the pandemic-fueled boom times would keep going, they aggressively expanded by hoarding the most fought-over and expensive resource in the software business: talent.

Silicon Valley tech companies have long seen hiring as more than just filling openings. The industry’s fierce talent wars showed that companies like Google and Meta were gaining the best and brightest. Ballooning staffs and a long reign atop lists of the most-desired jobs for college graduates were emblems of growth, deep pockets and prestige. And to employees, the work became something larger — it was an identity.

2) Activists have receipts

Like Blackwells did with Peloton, activist investors often go public with their criticisms. Many of them have done their homework.

In November, activist hedge fund TCI Fund Management, which holds a $6 billion stake in Alphabet, called on the company, in a public letter, to dramatically cut costs and reduce headcount:

You have publicly stated that Google should be 20% more efficient. We could not agree more. Nearly all technology companies are reducing costs. Meta reduced headcount by 13% last week. Amazon is reducing headcount by 10,000. Microsoft, Salesforce, Stripe and Twitter are also reducing headcount.

Alphabet's headcount has increased at an annual rate of 20% since 2017. It has more than doubled since 2017. This growth is excessive, both in relation to historic headcount growth and what the business requires.

TCI also called on the company to lower compensation:

Alphabet pays some of the highest salaries in Silicon Valley. As detailed in Alphabet's Schedule 14A filing, median compensation totaled $295,884 in 2021. An analysis by S&P Global illustrates that median compensation at Alphabet was 67% higher than at Microsoft and 153% higher than the 20 largest listed technology companies in the US. There is no justification for this enormous disparity.

We acknowledge that Alphabet employs some of the most talented and brightest computer scientists and engineers, but these represent only a fraction of the employee base. Many employees are performing general sales, marketing and administrative jobs, who should be compensated in-line with other technology companies.

Cost-cutting was also the theme of Altimeter Capital’s public letter to Meta in October:

But Meta needs to get its mojo back. Meta needs to re-build confidence with investors, employees and the tech community in order to attract, inspire, and retain the best people in the world. In short, Meta needs to get fit and focused.

To accomplish this goal, we recommend a three step plan that will double FCF to $40 B per year and focus the company’s teams and investments:

Reduce headcount expense by at least 20%;

Reduce annual capex by at least $5 B from $30B to $25B; and

Limit investment in metaverse / Reality Labs to no more than $5B per year.

3) Cheap stocks are attractive for activists

The data is mixed on whether activist campaigns are more or less prevalent during recessions. On the one hand, stocks are cheaper, and amassing bigger equity stakes is less costly. On the other hand, a bear market makes it harder to have confidence in the ability to turn around a single company amidst a broader decline. I’d also bet that many activist investors, who make their money by buying large amounts of equity, are sitting on some less-than-stellar portfolio returns based on 2022’s equity market performance. This could increase the pressure to launch fewer activist campaigns this year.

Yet, some of the biggest companies in tech, are so ripe for a shakeup, that even poor-performing activist investors will start aiming for them in 2023.

The S&P 500 is down 16% over the past year while the NASDAQ is down nearly 30% over the same period. The aforementioned tech heavyweights of their comparables have seen some of the largest declines in shareholder value ever.

Here are a few companies I expect to spend at least part of 2023 fending off activist investors:

Tesla. The most obvious activist target is Tesla. The veil has been lifted on Elon Musk, who seems intent on destroying the financial prospects of two companies. Tesla’s stock is down more than 66% in the past year while Elon micromanages everything at Twitter. Tesla fended off a number of activist proposals last year, but one approved proposal will allow large shareholders to nominate alternate members to Tesla’s board, which has all the trappings of a CEO fiefdom.

Alphabet. TCI fired the first shot, but the existential threat posed by ChatGPT/OpenAI and Microsoft to Google’s search business could embolden activist shareholders to push harder for the company to refocus on priorities or more quickly defend its territory.

Disney. The world’s second-largest media company is currently in a battle with Trian Fund Management, an activist hedge fund that owns an $800 million stake. The surprise return of CEO Bob Iger in November, exposed weak leadership at the board level, which may pose new opportunities for activists to pounce.

I’m making 10 predictions for 2023. Read my others below.